Good news continues to emerge on energy use and we may be reaching a tipping point where world CO2 emissions globally start to decline. Although too early to be sure the signs are very encouraging.

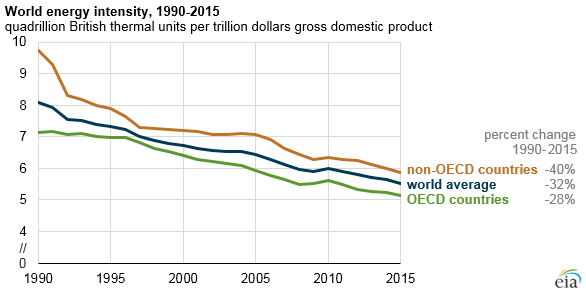

One pleasing aspect is China, which experienced the largest increase in energy productivity - by 133%. This means for the 15 year period from 1990 to 2015 the amount of energy used per unit of GDP (Note 1) has been rapidly declining. Put another way total emissions can reduce notwithstanding continuing increases in GDP. In other words China can simultaneously drastically reduce total carbon emissions yet still grow at a decent clip.

China presently accounts for 30 per cent of global carbon emissions, but pledged to cap its emissions by 2030 at the Paris summit. But according to more recent data from Earth Systems Science, indicative of far less coal usage, the likelihood is this cap may already have occurred.

This study published by Earth System Science Data contends global CO2 emissions from fossil fuels and industry is projected to grow by just 0.2 per cent this year. What their more recent data shows is that world emissions remained constant at 36 billion metric tonnes over the past 2 years despite increases in GDP.

Hence the worrying nexus between economic gains, (more particularly in China) and inevitable emissions growth has been severed. Another important point to note is that regardless of government policies both individuals and business alike are increasingly moving to carbon abatement or it's elimination.

In fact for most boards of directors of larger entities there is concern over the sustainability of any investments reliant or supportive of fossil fuels. The fear is of a future class action by shareholders.

It doesn't mean one can become complacent, since the build up in CO2 continues, but it does mean we may have reached a tipping point to the extent total emissions could fall heavily in the decades ahead to avoid the catastrophic outcomes predicted.

Global energy intensity continues to decline

One pleasing aspect is China, which experienced the largest increase in energy productivity - by 133%. This means for the 15 year period from 1990 to 2015 the amount of energy used per unit of GDP (Note 1) has been rapidly declining. Put another way total emissions can reduce notwithstanding continuing increases in GDP. In other words China can simultaneously drastically reduce total carbon emissions yet still grow at a decent clip.

China presently accounts for 30 per cent of global carbon emissions, but pledged to cap its emissions by 2030 at the Paris summit. But according to more recent data from Earth Systems Science, indicative of far less coal usage, the likelihood is this cap may already have occurred.

This study published by Earth System Science Data contends global CO2 emissions from fossil fuels and industry is projected to grow by just 0.2 per cent this year. What their more recent data shows is that world emissions remained constant at 36 billion metric tonnes over the past 2 years despite increases in GDP.

Hence the worrying nexus between economic gains, (more particularly in China) and inevitable emissions growth has been severed. Another important point to note is that regardless of government policies both individuals and business alike are increasingly moving to carbon abatement or it's elimination.

In fact for most boards of directors of larger entities there is concern over the sustainability of any investments reliant or supportive of fossil fuels. The fear is of a future class action by shareholders.

It doesn't mean one can become complacent, since the build up in CO2 continues, but it does mean we may have reached a tipping point to the extent total emissions could fall heavily in the decades ahead to avoid the catastrophic outcomes predicted.

Global energy intensity continues to decline

Source: EIA, International Energy Outlook 2016, International Energy Statistics, and Oxford Economics

Note: OECD is the Organization for Economic Cooperation and Development. (1) GDP is gross domestic product . In other words all the goods and services produced in an economy.

Note: OECD is the Organization for Economic Cooperation and Development. (1) GDP is gross domestic product . In other words all the goods and services produced in an economy.

6 comments:

This is really hopeful Lindsay. Oddly, I think the new US Administration's ostrich head in the sand on climate change may spark leadership elsewhere. It's not very useful in the longer term to the US economy either, but that's another story. Here in Canada we have a commitment for a national carbon tax (our province has had one for years) - starting at $30 a ton and increasing over time.

That is good news, Lindsay. Having lived in the US as long as I did I tend to see worse news than may be entirely necessary. Of course it's also true we did pass the 400 ppm very dangerous level of CO2 last summer and methane is being released by the ton from melting permafrost. Unfortunately, for far too many there's more money to be made by ignoring the consequences of continuing recent practices.

I'm keeping my fingers crossed.

All the best.

Some very welcome good news, and this is very encouraging.

From what I have seen though, China procured a supply of anthracite from the Appalachian states, and will now be producing high-grade steels; the thought of which raises concerns on a number of points.

I fear the data cited may prove of limited utility in forecasts of the future.

Additionally, my warm fuzzies are a bit stilted by the fact that I tend to view a government as one of the most untrustworthy institutions known to man. Not sure if this effect is caused by being an American, or the stereotypical Gen-X thing I have going.

Nonetheless, any spot of hope on this point is a dear welcome.

Hi Gary

I was also pleasantly surprised at not only the outcomes here but also the more recent information I only gained over the past few days. That information points to an acceleration of those favorable trends. I agree the new US Administration's ostrich head in the sand approach will indeed spark leadership elsewhere. But it’s also true increasingly large swathes of the private sector couldn’t care less what he said because it doesn’t make any commercial sense to travel down the carbon road for them. As I said there is the risk of class actions by increasingly savvy investors against any management who invest or subject the enterprise to dependence on fossil fuels. Having an emissions of carbon tax scheme set at $30 a ton and increasing over time is the best way to incentivize investments away from the carbon emitters.

best wishes

Hi Susan

True – but only to increasingly smaller pockets of the economy who make money from the carbon heavy sectors. Mostly it doesn’t make much business sense as I commented to Gary. The problem is as you know even if we did achieve 100% to renewables to-day there still would be some global increases for a while. But I guess what’s emerging is there is no reason to believe that 100% target couldn’t be reached within the next 25- 50 years for renewables so the outcome won’t be good but nowhere near the catastrophic outcome that otherwise might otherwise ensue given no action was taken. Some of our states are already up to 50% but base power availability is a problem with recent blackouts when solar and wind aren’t generating enough power during hot days or if storms effect the traditional grid.

Best wishes

Hi Mercutio,

One of the pleasing aspects was the marked diminution in Chinese emissions per GDP and we are about to see this trend accelerate markedly. The reason being Chinese steel exports for the past 4 or 5 years have acted as a kind of shock absorber to keep local production stable and flat in terms of production notwithstanding ever growing industry over-capacity. As the authorities continue their pragmatic approach to curtail exports and improve outcomes on the domestic economy, industry rationalizations are accelerating. Bear in mind there is far less timidity then would apply to the west, to modernize rust bucket regions nor a propensity to blame someone else or resort to protectionary policies. Instead the authorities have no hesitation in taking a somewhat brutal approach which would politically impossible elsewhere.

Hence these moves to add efficiencies and eliminate costly over-capacity will add significantly to the existing downward global trend.

But this is having a perverse short term effect of increasing the spot prices for high grade iron ore and coal. The reason is more emphasis is being placed on procurement of the higher quality inputs because you are able immediately to improve efficiencies. The end result in a corresponding sharp fall in emissions and smog, which is just what the authorities and the general population want to see. But the spike in prices will be short lived since overall demand is going to continue to diminish in the decades ahead. Those on the supply side building in new capacity are going to get burnt.

From what I know about Anthracite coal it is only a very small portion of coal in general but has the advantage of much higher efficiencies and a corresponding higher energy output per its weight. It also burns much more cleanly with less soot, compared to all other coal varieties. The mountainous region to which you refer no doubt produces a high quality variety and hence it makes sense for the Chinese to import and close down ageing less efficient plants in China.

Best wishes

Post a Comment